The number of cable homes in Europe reached 69.2 million in 2017, or 36.3% of all TV households, in 2017. This, according to the European Broadband Cable Yearbook from IHS Markit and Cable Europe, was the highest number since 2009, when the figure stood at 70 million.

The number of cable homes in Europe reached 69.2 million in 2017, or 36.3% of all TV households, in 2017. This, according to the European Broadband Cable Yearbook from IHS Markit and Cable Europe, was the highest number since 2009, when the figure stood at 70 million.

Key findings of the new 2018 edition of the Yearbook, which is the only industry report supported by Cable Europe, include the following:

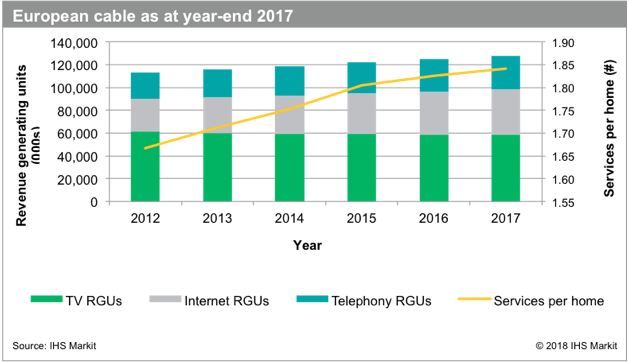

Total revenue generating units (RGUs) rose 2 % year on year to 127.5 million, largely driven by an increase in internet subscriptions

At the end of 2017, cable customers in Europe subscribed to an average of 1.8 services.

TV services accounted for 46% of cable TV revenue in 2017, followed by internet with 35% and telephony with 19%.

Germany continued to be the largest cable TV market in Europe, with 18.7 million subscribers, which was more than three times the number of unique subscribers in the next biggest markets of Romania, the UK and Poland

Annual total cable revenue continued the steady growth path set in 2010, reaching €25.9 billion last year, up 2% compared to 2016. In terms of revenue growth, internet was the best-performing cable category, with revenue rising 4% to €9 billion in 2017.

Commenting on the findings of the Yearbook, Maria Rua Aguete, executive director of media, service providers and platforms for IHS Markit, said: “Broadband internet is a key factor in European cable TV revenue growth.

“Triple-play and quad-play strategies are also being implemented. They strengthen operators’ status as a multi-platform point to anytime, anywhere content.”

Telephony revenue contracted for the second consecutive year, declining 0.7% to €5 billion. Revenues for VOD services increased in 2017, returning to growth following the category’s minor downturn between 2012 and 2014. Average monthly revenue per subscriber (ARPU) last year was €16.79 for TV, €19.59 for internet and €14.35 for telephony.

The total number of cable TV service subscribers in Europe in 2017 remained flat at 58.9 million.

Martyn Hannant, research and analysis manager, IHS Markit, added: “The European cable industry continues to show resilience.

“The industry has made significant progress in the switchover from analogue to digital cable signals”.

The rate of digitisation of European cable TV homes grew in 2017. As the digital switchover gathered momentum, the number of digital subscribers grew 13% compared to 2016. A significant portion of this growth came from Germany’s Unitymedia, which switched off its analogue TV signals in July 2017.

Mergers and acquisitions were once again a key characteristic of the European cable industry last year, including the sale of UPC Austria to T-Mobile Austria, Telenet’s purchase of Altice’s SFR Belux and Euskaltel’s acquisition of Telecable. However, these deals were somewhat eclipsed by the €18.4 billion Liberty Global agreement to sell key European assets to Vodafone in Germany, Hungary, Romania and the Czech Republic.

Cable operators also made further enhancements to their services last year. For instance, German companies launched advanced TV services, including the rollout of the Vodafone GigaTV service and the Tele Colombus introduction of AdvanceTV. Both services crucially incorporated 4K capabilities.

The use of Android TV for interactive TV services also became increasingly popular in Europe last year, as DNA in Finland and YouSee in Denmark both launched Android TV products.